Dr. Einav is a professor of economics at Stanford. Dr. Finkelstein is a professor of economics at the Massachusetts Institute of Technology.

There is no shortage of proposals for health insurance reform, and they all miss the point. They invariably focus on the nearly 30 million Americans who lack insurance at any given time. But the coverage for the many more Americans who are fortunate enough to have insurance is deeply flawed.

Health insurance is supposed to provide financial protection against the medical costs of poor health. Yet many insured people still face the risk of enormous medical bills for their “covered” care. A team of researchers estimated that as of mid-2020, collections agencies held $140 billion in unpaid medical bills, reflecting care delivered before the Covid-19 pandemic. To put that number in perspective, that’s more than the amount held by collection agencies for all other consumer debt from nonmedical sources combined. As economists who study health insurance, what we found really shocking was our calculation that three-fifths of that debt was incurred by households with health insurance.

What’s more, in any given month, about 11 percent of Americans younger than 65 are uninsured. But more than twice that number — one in four — will be uninsured for at least some time over a two-year period. Many more face the constant danger of losing their coverage. Perversely, health insurance — the very purpose of which is to provide a measure of stability in an uncertain world — is itself highly uncertain. And while the Affordable Care Act substantially reduced the share of Americans who are uninsured at a given time, we found that it did little to reduce the risk of insurance loss among the currently insured.

It’s tempting to think that incremental reforms could address these problems. For example, extend coverage to those who lack formal insurance. Make sure all insurance plans meet some minimum standards. Change the laws so that people don’t face the risk of losing their health insurance coverage when they get sick, when they get well (yes, that can happen) or when they change jobs, give birth or move.

But those incremental reforms won’t work. Over a half-century of such well-intentioned, piecemeal policies has made clear that continuing this approach represents the triumph of hope over experience, to borrow a description of second marriages commonly attributed to Oscar Wilde.

The risk of losing coverage is an inevitable consequence of a lack of universal coverage. Whenever there are varied pathways to eligibility, there will be many people who fail to find their path.

About six in 10 uninsured Americans are eligible for free or heavily discounted insurance coverage. Yet they remain uninsured. Lack of information about which of the array of programs they are eligible for, along with the difficulties of applying and demonstrating eligibility, mean that the coverage programs are destined to deliver less than they could.

The only solution is universal coverage that is automatic, free and basic.

Automatic because when we require people to sign up, not all of them do. The experience with the health insurance mandate under the Affordable Care Act makes that clear.

Coverage needs to be free at the point of care — no co-pays or deductibles — because leaving patients on the hook for large medical costs is contrary to the purpose of insurance. A natural rejoinder is to go for small co-pays — a $5 co-pay for prescription drugs or $20 for a doctor visit — so that patients make more judicious choices about when to see a health care professional. Economists have preached the virtues of this approach for generations.

But it turns out there’s an important practical wrinkle with asking patients to pay even a very small amount for some of their universally covered care: There will always be people who can’t manage even modest co-pays. Britain, for example, introduced co-pays for prescription drugs but then also created programs to cover those co-pays for most patients — the elderly, young, students, veterans and those who are pregnant, low-income or suffering from certain diseases. All told, about 90 percent of prescriptions are exempted from the co-pays and dispensed free. The net result has been to add hassles for patients and administrative costs for the government, with little impact on the patients’ share of total health care costs or total national health care spending.

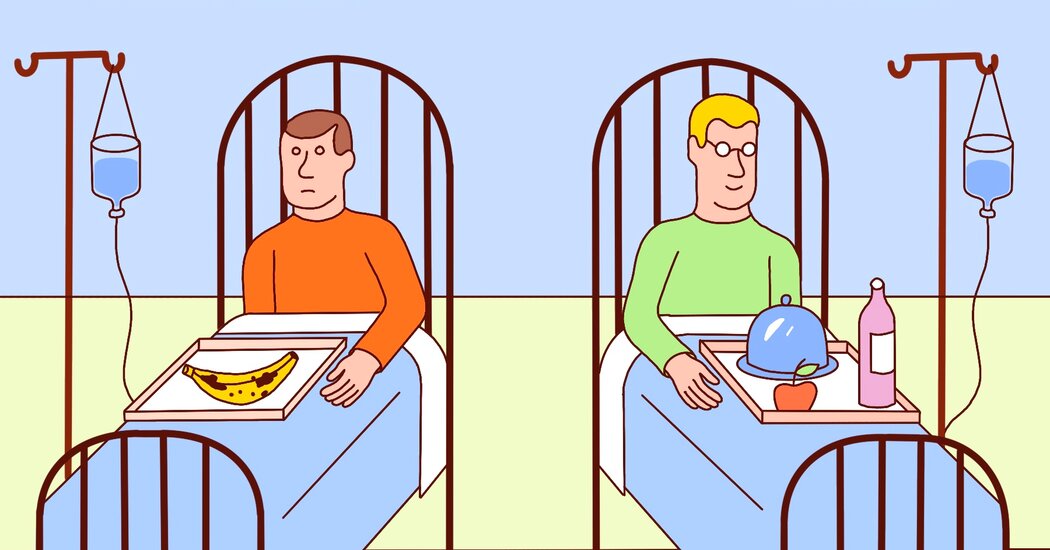

Finally, coverage must be basic because we are bound by the social contract to provide essential medical care, not a high-end experience. Those who can afford and want to can purchase supplemental coverage in a well-functioning market.

Here, an analogy to airline travel may be useful. The main function of an airplane is to move its passengers from point A to point B. Almost everyone would prefer more legroom, unlimited checked bags, free food and high-speed internet. Those who have the money and want to do so can upgrade to business class. But if our social contract were to make sure everyone could fly from A to B, a budget airline would suffice. Anyone who’s traveled on one of the low-cost airlines that have transformed airline markets in Europe knows it is not a wonderful experience. But they do get you to your destination.

Keeping universal coverage basic will keep the cost to the taxpayer down as well. It’s true that as a share of its economy, the United States spends about twice as much on health care as other high-income countries. But in most other wealthy countries, this care is primarily financed by taxes, whereas only about half of U.S. health care spending is financed by taxes. For those of you following the math, half of twice as much is … well, the same amount of taxpayer-financed spending on health care as a share of the economy. In other words, U.S. taxes are already paying for the cost of universal basic coverage. Americans are just not getting it. They could be.

We arrived at this proposal by using the approach that comes naturally to us from our economics training. We first defined the objective, namely the problem we are trying but failing to solve with our current U.S. health policy. Then we considered how best to achieve that goal.

Nonetheless, once we did this, we were struck — and humbled — to realize that at a high level, the key elements of our proposal are ones that every high-income country (and all but a few Canadian provinces) has embraced: guaranteed basic coverage and the option for people to purchase upgrades.

The lack of universal U.S. health insurance may be exceptional. The fix, it turns out, is not.

Also if you’re quick, before NYTimes pops up it’s “subscribe” window, you can hit Ctrl-A and Ctrl-C to copy all the text from the article… which is how I got the text from my previous post.

Lol I pay for NYTimes but they consistently want me to login and hit buttons before I can read an article so I usually end up just bypassing their paywall because it is easier.

I also pay for the NYT and I just love getting full page ads multiple times in the articles I paid to read. Sometimes it’s the SAME full page ad five times in a row, just in case I missed the previous 4 copies!

Lack of universal coverage. The piece argues that the only solution is universal coverage that is automatic, free and basic. The current U.S. system has many pathways to eligibility and coverage, resulting in many people falling through the cracks and remaining uninsured.

Incremental reforms are not enough. The authors argue that incremental reforms like extending coverage to more people or imposing minimum standards will not work. Over 50 years of such piecemeal policies have shown that this approach is not effective.

Coverage is complex and uncertain. Health insurance in the U.S. is complex, with many different plans and eligibility requirements. This leads to many people losing coverage or facing the risk of losing it. Even the Affordable Care Act did little to reduce this uncertainty.

Cost. While the U.S. spends more on health care as a percentage of GDP, only about half of that spending is financed through taxes. The authors argue that U.S. taxes are already paying for the cost of a universal basic coverage system, but Americans are not getting it.

The trouble is, none of those are the real reason, which is that the ruling class wants it to have all those “problems” because increasing the risk and cost of people changing jobs helps suppress wages.

You’d think a couple of ivy-league professors of economics would’ve figured that out. So why didn’t they mention it?

Good question. I know this is an unpopular opinion but maybe… they are actual subject matter experts and you’re not?

I know, blaming a group of evil people is tempting, easier to understand and more satisfying that than a complex system of misaligned incentives grown organically through many decades of well intentioned but ineffective measures. Not that I know much about it, but, you know, conspiracy theories tend not to be true.

Because their arguments can be made empirically and therefore justified. Please find me a member of the ruling elite who will admit what you just proposed. No evidence, no change

I get the feeling we didn’t read the article in the same way. I didn’t see any excuse making for American exceptionalism at all.

At the very end it points out the essential flaw that Americans are already paying for basic health care but not receiving it.

Article text :

By Liran Einav and Amy Finkelstein

Dr. Einav is a professor of economics at Stanford. Dr. Finkelstein is a professor of economics at the Massachusetts Institute of Technology.

There is no shortage of proposals for health insurance reform, and they all miss the point. They invariably focus on the nearly 30 million Americans who lack insurance at any given time. But the coverage for the many more Americans who are fortunate enough to have insurance is deeply flawed.

Health insurance is supposed to provide financial protection against the medical costs of poor health. Yet many insured people still face the risk of enormous medical bills for their “covered” care. A team of researchers estimated that as of mid-2020, collections agencies held $140 billion in unpaid medical bills, reflecting care delivered before the Covid-19 pandemic. To put that number in perspective, that’s more than the amount held by collection agencies for all other consumer debt from nonmedical sources combined. As economists who study health insurance, what we found really shocking was our calculation that three-fifths of that debt was incurred by households with health insurance.

What’s more, in any given month, about 11 percent of Americans younger than 65 are uninsured. But more than twice that number — one in four — will be uninsured for at least some time over a two-year period. Many more face the constant danger of losing their coverage. Perversely, health insurance — the very purpose of which is to provide a measure of stability in an uncertain world — is itself highly uncertain. And while the Affordable Care Act substantially reduced the share of Americans who are uninsured at a given time, we found that it did little to reduce the risk of insurance loss among the currently insured.

It’s tempting to think that incremental reforms could address these problems. For example, extend coverage to those who lack formal insurance. Make sure all insurance plans meet some minimum standards. Change the laws so that people don’t face the risk of losing their health insurance coverage when they get sick, when they get well (yes, that can happen) or when they change jobs, give birth or move.

But those incremental reforms won’t work. Over a half-century of such well-intentioned, piecemeal policies has made clear that continuing this approach represents the triumph of hope over experience, to borrow a description of second marriages commonly attributed to Oscar Wilde.

The risk of losing coverage is an inevitable consequence of a lack of universal coverage. Whenever there are varied pathways to eligibility, there will be many people who fail to find their path.

About six in 10 uninsured Americans are eligible for free or heavily discounted insurance coverage. Yet they remain uninsured. Lack of information about which of the array of programs they are eligible for, along with the difficulties of applying and demonstrating eligibility, mean that the coverage programs are destined to deliver less than they could.

The only solution is universal coverage that is automatic, free and basic.

Automatic because when we require people to sign up, not all of them do. The experience with the health insurance mandate under the Affordable Care Act makes that clear.

Coverage needs to be free at the point of care — no co-pays or deductibles — because leaving patients on the hook for large medical costs is contrary to the purpose of insurance. A natural rejoinder is to go for small co-pays — a $5 co-pay for prescription drugs or $20 for a doctor visit — so that patients make more judicious choices about when to see a health care professional. Economists have preached the virtues of this approach for generations.

But it turns out there’s an important practical wrinkle with asking patients to pay even a very small amount for some of their universally covered care: There will always be people who can’t manage even modest co-pays. Britain, for example, introduced co-pays for prescription drugs but then also created programs to cover those co-pays for most patients — the elderly, young, students, veterans and those who are pregnant, low-income or suffering from certain diseases. All told, about 90 percent of prescriptions are exempted from the co-pays and dispensed free. The net result has been to add hassles for patients and administrative costs for the government, with little impact on the patients’ share of total health care costs or total national health care spending.

Finally, coverage must be basic because we are bound by the social contract to provide essential medical care, not a high-end experience. Those who can afford and want to can purchase supplemental coverage in a well-functioning market.

Here, an analogy to airline travel may be useful. The main function of an airplane is to move its passengers from point A to point B. Almost everyone would prefer more legroom, unlimited checked bags, free food and high-speed internet. Those who have the money and want to do so can upgrade to business class. But if our social contract were to make sure everyone could fly from A to B, a budget airline would suffice. Anyone who’s traveled on one of the low-cost airlines that have transformed airline markets in Europe knows it is not a wonderful experience. But they do get you to your destination.

Keeping universal coverage basic will keep the cost to the taxpayer down as well. It’s true that as a share of its economy, the United States spends about twice as much on health care as other high-income countries. But in most other wealthy countries, this care is primarily financed by taxes, whereas only about half of U.S. health care spending is financed by taxes. For those of you following the math, half of twice as much is … well, the same amount of taxpayer-financed spending on health care as a share of the economy. In other words, U.S. taxes are already paying for the cost of universal basic coverage. Americans are just not getting it. They could be.

We arrived at this proposal by using the approach that comes naturally to us from our economics training. We first defined the objective, namely the problem we are trying but failing to solve with our current U.S. health policy. Then we considered how best to achieve that goal.

Nonetheless, once we did this, we were struck — and humbled — to realize that at a high level, the key elements of our proposal are ones that every high-income country (and all but a few Canadian provinces) has embraced: guaranteed basic coverage and the option for people to purchase upgrades.

The lack of universal U.S. health insurance may be exceptional. The fix, it turns out, is not.

Also if you’re quick, before NYTimes pops up it’s “subscribe” window, you can hit Ctrl-A and Ctrl-C to copy all the text from the article… which is how I got the text from my previous post.

Lol I pay for NYTimes but they consistently want me to login and hit buttons before I can read an article so I usually end up just bypassing their paywall because it is easier.

I also pay for the NYT and I just love getting full page ads multiple times in the articles I paid to read. Sometimes it’s the SAME full page ad five times in a row, just in case I missed the previous 4 copies!

We need a bot that auto replies to URL posts to certain domains with light paywalls to https://archive.is/<URL>

You can also use reader view.

Though it seems a bit trial-and-error. Scroll down a bit (so it actually loads the text) then hit the reader icon.

Take THAT!

Summarized: So why don’t they have it?

The trouble is, none of those are the real reason, which is that the ruling class wants it to have all those “problems” because increasing the risk and cost of people changing jobs helps suppress wages.

You’d think a couple of ivy-league professors of economics would’ve figured that out. So why didn’t they mention it?

Good question. I know this is an unpopular opinion but maybe… they are actual subject matter experts and you’re not?

I know, blaming a group of evil people is tempting, easier to understand and more satisfying that than a complex system of misaligned incentives grown organically through many decades of well intentioned but ineffective measures. Not that I know much about it, but, you know, conspiracy theories tend not to be true.

Because their arguments can be made empirically and therefore justified. Please find me a member of the ruling elite who will admit what you just proposed. No evidence, no change

deleted by creator

I get the feeling we didn’t read the article in the same way. I didn’t see any excuse making for American exceptionalism at all. At the very end it points out the essential flaw that Americans are already paying for basic health care but not receiving it.